The Sold-Out Air Conditioner Factory Quietly Building a Global Robotics Empire

Unusual Stocks is a Sunday series about public companies most people have never considered as investments. Some are strange businesses. Some are in strange places. All of them are worth knowing about.

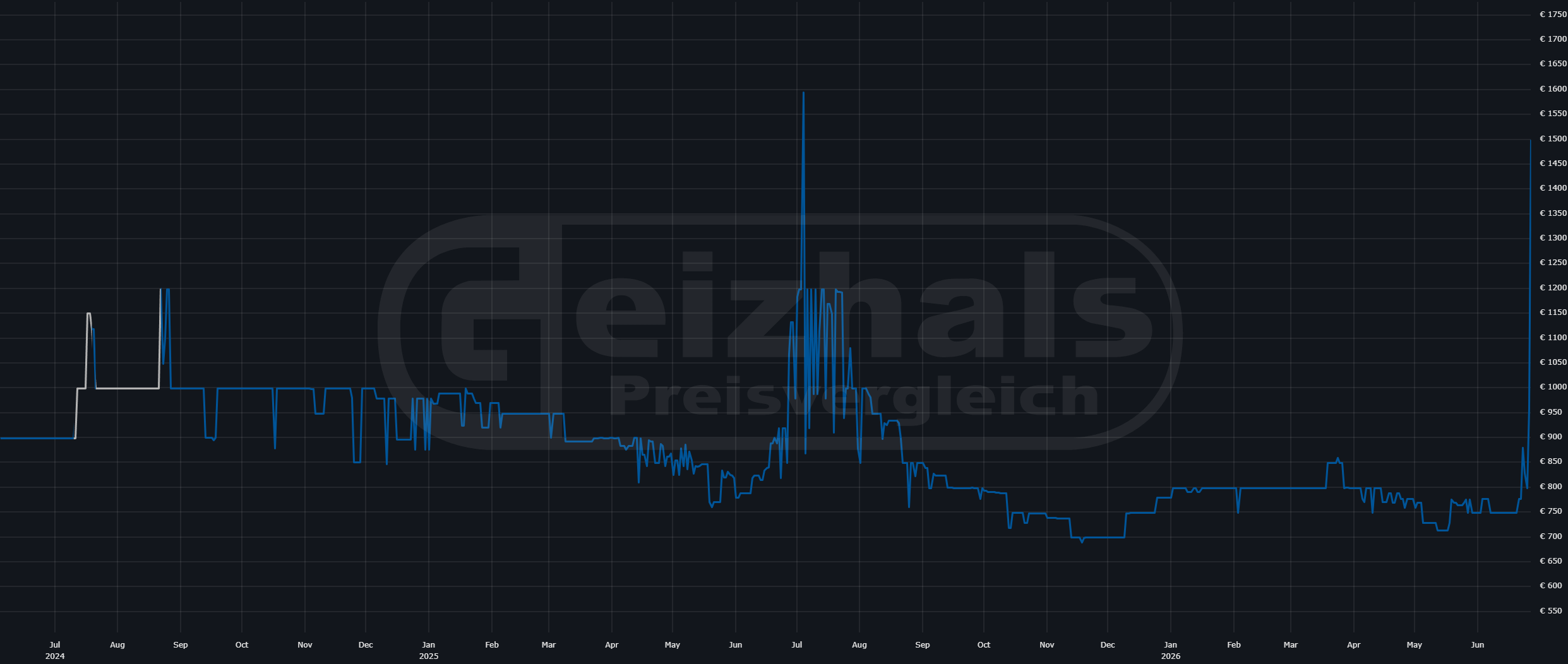

Right now, somewhere in Germany, someone is refreshing a price tracker at midnight hoping a Midea PortaSplit portable air conditioner drops back down to reality. They won’t find one at standard retail. Driven by a severe European heatwave, tech platforms confirm the unit is virtually sold out across multiple countries and completely unavailable on Amazon. Units that normally retail between €750 and €800 are currently listed for as much as €2,995, and the absolute cheapest option on eBay right now sits at a stinging €2,000.

This isn’t just a temporary weather anomaly; it is a massive logistics sprint. Midea’s factories in Guangdong are working around the clock to rush inventory to Europe via freight trains. In regions with historically low air conditioner penetration, specifically Germany, France, Spain, and the UK, Midea’s sales have skyrocketed, posting a year-on-year increase of more than 70 percent.

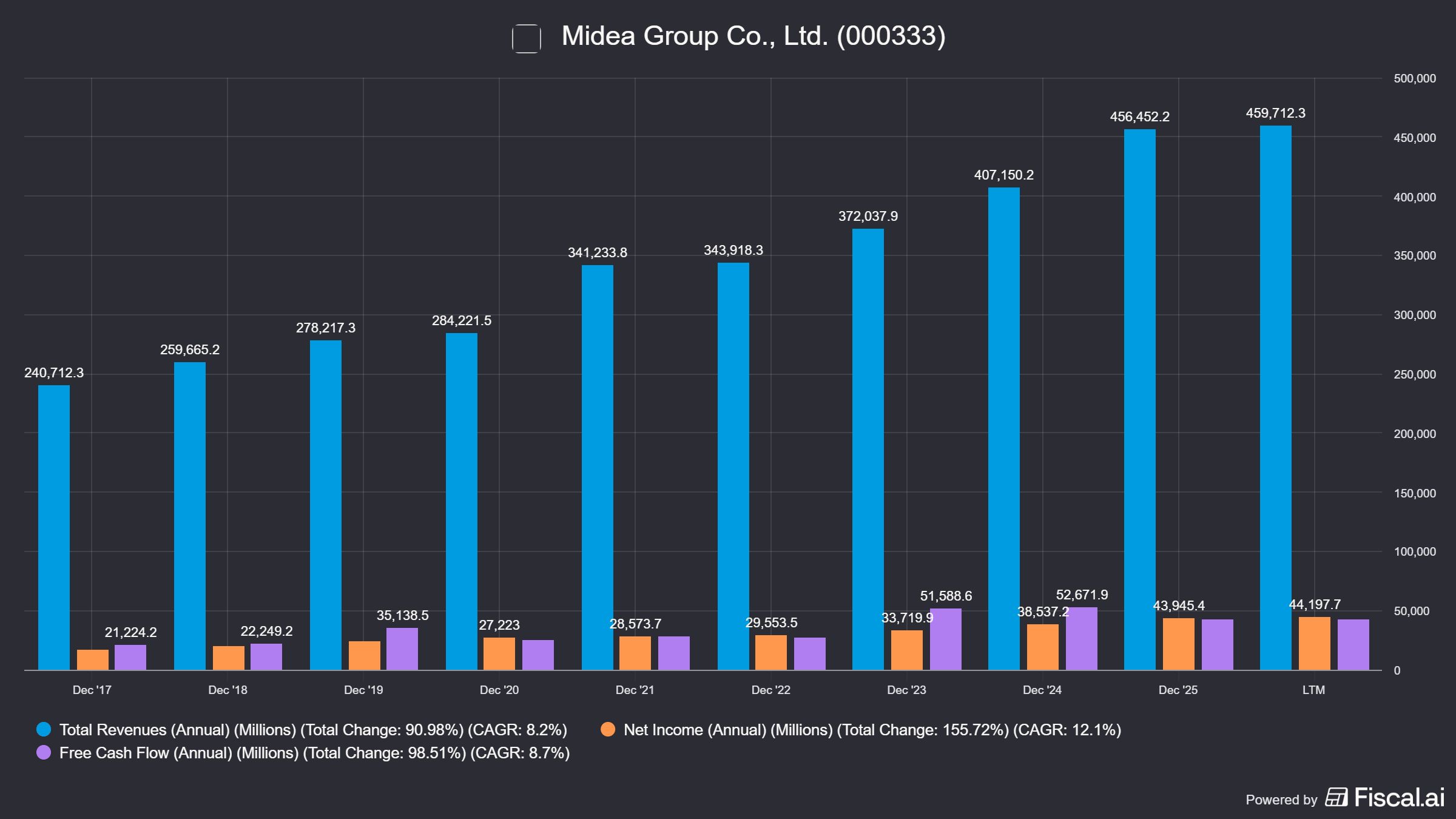

Before you write this off as a one-quarter weather story, look at the underlying financial machine. In 2025, Midea generated RMB 459.71 billion in revenue and RMB 43.95 billion in net profit. Overseas revenue reached RMB 195.9 billion, up 16% year over year. The company runs localized operations in 50 countries, with 29 overseas R&D centers and 43 overseas manufacturing bases.

In most professional investing circles, mention Midea and you’ll get a shrug. Most investors simply see a massive, low-margin Chinese appliance maker and stop reading. That is exactly why it fits the Unusual Stocks profile. The ones who kept reading would find a company that has quietly become one of the largest industrial robotics players on earth, a controlling shareholder in a Toshiba elevator business, and the single biggest beneficiary of a continent that just discovered it needs air conditioning.

The Consumer Machine (Smart Home)

The unglamorous fact underneath Midea’s consumer business, known officially as Smart Home, is that it doesn’t just make air conditioners. It makes nearly everything that plugs in: refrigerators, washing machines, microwaves, and small kitchen appliances. Midea is a top three player by retail sales in most home appliance categories in China, and it is one of the few companies that actually manufacture the world’s air conditioners. China accounts for more than half of global AC production capacity, and Midea owns a meaningful chunk of it.

That scale is the moat, and Europe is currently proving it in real time. Only about 20% of European households own an air conditioner today, against roughly 90% in the United States. That gap is not a one-off. It is a multi-decade adoption curve accelerated by a massive structural loophole: the European rental market.

In countries like Germany, over half the population rents their homes. Installing a traditional fixed-split AC requires drilling through exterior walls, which needs the landlord's permissions. The PortaSplit is a product-market fit masterpiece because it requires zero drilling and zero landlord approval, bypassing the red tape while still delivering almost split-system performance.

The manufacturer best positioned to ride this adoption curve doesn’t have to compete with a domestic European AC industry, because there isn’t much of one left to compete with.

The Regulatory Tailwind Nobody’s Pricing In

There's a second tailwind sitting underneath the heatwave headlines, and it's structural rather than seasonal. The EU's F-Gas Regulation is forcing a phase-out of high global warming potential refrigerants across the bloc's HVAC industry. Midea just crossed ten million units sold worldwide of its R290 air conditioners, which run on a natural, low-GWP refrigerant. The company has now held the top spot globally in R290 air conditioners for three consecutive years, according to Euromonitor. The rollout has successfully avoided roughly 5.2 million tonnes of CO2 equivalent emissions to date, earning the brand environmental accolades like the "Blue Angel" mark.

The harder part of that transition isn't manufacturing the units. It is training a continent's worth of installers to handle a different refrigerant safely. Midea has spent fifteen years building leak prevention and fire safety systems around R290. As an official member of the UN Global Compact, it runs installer training partnerships in tight markets like Malta, where a yearlong program with local provider KENKAR safely deployed 240 units without safety incidents. That's the kind of unglamorous, capital-intensive groundwork a smaller competitor can't easily replicate on short notice, right as European regulation makes it mandatory.

The Second Curve: The Business Machine (ToB)

The more interesting part of Midea isn’t the appliances, though. It is everything the company has bolted on around them, expanding its industrial reach across defined business units:

Robotics & Automation: Anchored by KUKA, the German industrial robot heavyweight Midea acquired in 2016.

Building Technologies: Expanded via a controlling 58% stake in Toshiba Elevator’s China operations and the acquisition of Arbonia’s climate division, now combined under the MBT Climate alliance.

Industrial Technology: Pumping out high-precision climate components, compressors, and automotive parts.

Midea Energy: Providing system integration across grid-scale, commercial, and residential energy storage systems.

Midea Healthcare: Driving medical imaging technology innovations.

ANNTO: Managing end-to-end digital, intelligent supply chain networks.

Professional Platforms: Housing focused financial business operations and advanced AI Research Centers.

This commercial machine hit RMB 122.8 billion in revenue during 2025, up 17.5% year over year, representing 27% of total revenue and out-pacing the retail growth.

The latest Q1 2026 earnings report shows this multi-engine machine navigating mixed segment performance. Building Technologies grew 10.1% year over year to RMB 10.8 billion, and Robotics & Automation climbed 11.8% to RMB 8.2 billion. Conversely, Industrial Technology fell 11.7% to RMB 6.8 billion. Put plainly, the company selling you a window AC unit might also service the elevator in your office building and the robot arm on a factory floor, but not every part of that empire grows at the exact same pace.

The Numbers

Midea’s Q1 2026 report tells a more nuanced story than the 2025 annual letter does. Total quarterly revenue grew 2.55% year over year to RMB 131.1 billion, and net profit attributable to shareholders rose 2.03% to RMB 12.67 billion. Strip out non-recurring items, mostly fair value adjustments on financial assets and gains on asset disposals, and core profit fell 14.02% year over year to RMB 11.0 billion.

The cash flow statement shows where the movement came from. Operating cash flow was basically flat, up 1.45% to RMB 14.5 billion. But the company swung from a RMB 23.2 billion cash outflow on investing activities in Q1 2025 to a RMB 5.1 billion inflow in Q1 2026, largely from recovering cash tied up in financial investments rather than from immediate operating strength. Financing activities flipped from a RMB 7.3 billion inflow to a RMB 11.7 billion outflow, as the company focused on paying down debt. It is a company managing its balance sheet rather than blowing out its core earnings power this particular quarter.

On June 17, 2026, Midea executed a share repurchase of 3.1583 million A-shares, involving a total expenditure of approximately RMB 250 million. The overall balance sheet remains highly conservative, tracking a negative Net Debt position of -RMB 38.2 billion, meaning the business holds far more cash on hand (RMB 96.42 billion) than total debt.

The A Share, the H Share, and the China Risk

Midea’s shareholder base is a useful map of how money actually reaches this stock. Midea Holding, the vehicle aligned with the company’s founding family and senior management, controls about 28.5%. Hong Kong Securities Clearing and HKSCC Nominees, the two channels through which Stock Connect and H-share investors hold their stock, together account for more than 21% of shares. Chairman and CEO Fang Hongbo personally holds about 1.5%.

The primary listing, 000333, trades in renminbi on the Shenzhen exchange and is only directly accessible to foreign investors through Stock Connect or a qualified institutional license. The Hong Kong listing, 0300, trades in Hong Kong dollars and is open to ordinary international brokerage accounts, but it draws from a separate, smaller pool of shares. A shares and H shares of the same company routinely trade at different prices because the investor bases on either side of the border aren’t the same people. On top of that, every quarterly report Midea files, including the Q1 2026 numbers above, carries an explicit disclosure that the figures are unaudited. That’s standard practice under Chinese listing rules, not a red flag specific to Midea, but it’s a real difference from the audited quarterly filings investors are used to seeing out of the US or UK.

Then there's the macro overlay. Midea now earns 43% of revenue outside China, which cuts geopolitical risk relative to a pure domestic appliance maker, but it also means tariff policy and trade tension between China and its biggest export markets is a real input into the model rather than a hypothetical one.

The Price Tag

At a market cap of roughly RMB 587 billion, Midea trades at about 13.7 times trailing earnings and 10.5 times EV to EBITDA, against a return on equity that has averaged 20.1% over the past five years. That’s a cheap multiple for that kind of return on capital. The dividend yield, currently around 5.5%, comes with a payout ratio that has climbed to 73.6% of earnings, and dividend per share has grown comfortably alongside the high single-digit growth in the underlying business.

The one number worth sitting with is this: consensus estimates call for EBITDA to shrink slightly over the next two years even as revenue keeps growing around 6% a year, which lines up with what the Q1 2026 core profit number is already showing. The market isn’t pricing Midea like a growth stock, and the company’s own most recent numbers suggest it shouldn’t be.

So you’re left with a fairly straightforward trade. You are not paying up for a growth story. You are paying a mid-teens multiple for a company that builds the air conditioner Europe currently can’t buy, holds the regulatory high ground on the refrigerant Europe is about to mandate, and quietly owns a piece of the robot arm bolting your next car together, all while accepting that its biggest shareholders, its accounting standards, and its export exposure all run through Beijing rather than Brussels or Washington.

Disclaimer

The information provided in this content is intended solely for educational and informational purposes. It is not financial, investment, or trading advice. I am not a licensed financial advisor, professional analyst, or registered with any securities regulator (e.g., SEC in the U.S., BaFin in Germany), and the views expressed are my personal opinions, not guarantees of future performance. Investing involves significant risks, including the potential loss of capital, and past performance does not predict future results. Any mention of potential benefits does not outweigh these risks and may not be suitable for your individual circumstances, risk profile, or needs.

You should conduct your own research or consult a licensed financial advisor before making any investment decisions, considering tax and securities laws in your jurisdiction (e.g., German capital gains tax, U.S. IRS rules). For binding advice, consult professionals in your jurisdiction, ideally in your local language. I am not responsible for any financial outcomes resulting from actions taken based on this content.

By engaging with this content, you acknowledge and agree that you are solely responsible for your own investment choices. I am not currently invested in any of the assets or securities discussed but reserve the right to buy or sell shares at any time without further notice. While all information is believed to be reliable and was prepared in good faith, its accuracy and completeness are not guaranteed.